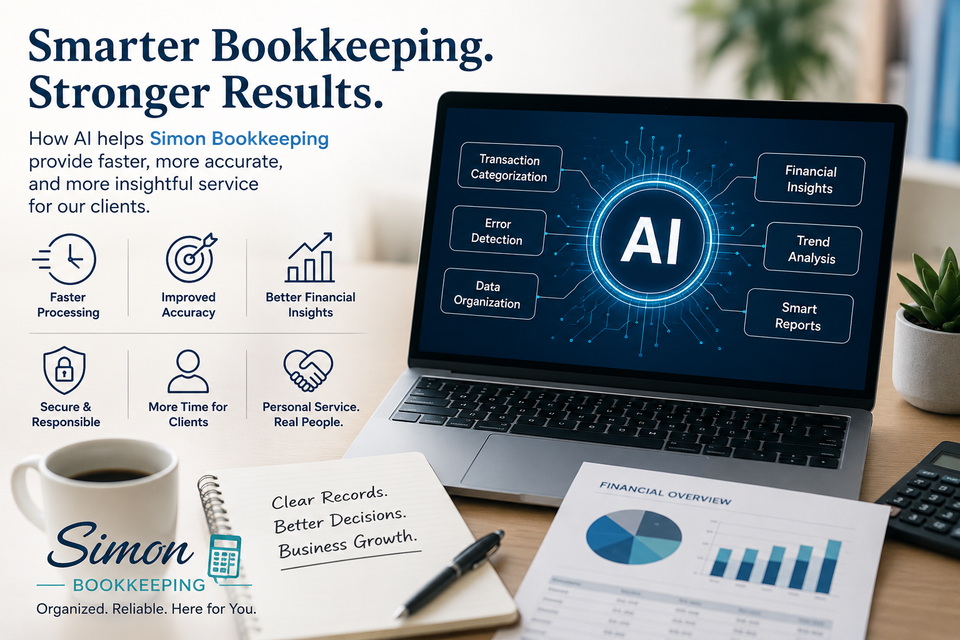

How Simon Bookkeeping Uses AI to Better Serve Clients

In today’s fast-moving business world, bookkeeping is no longer just about entering numbers into software. Modern technology has changed the way financial information is organized, reviewed, and managed. At Simon Bookkeeping, we embrace the responsible use of Artificial Intelligence (AI) tools to provide faster, more accurate, and more efficient service for our clients — while still keeping the personal attention and human judgment that businesses deserve.

What AI Means for Bookkeeping

Artificial Intelligence is not a replacement for professional bookkeeping. Instead, it is a powerful tool that helps streamline repetitive tasks, improve organization, and uncover useful insights more quickly.

By combining AI-powered technology with real bookkeeping expertise, Simon Bookkeeping can focus more time on what truly matters:

- Helping clients understand their finances

- Catching potential issues early

- Improving accuracy

- Saving business owners valuable time

How Simon Bookkeeping Uses AI

Faster Transaction Organization

AI-assisted bookkeeping tools can help recognize and categorize transactions more efficiently. This speeds up data processing and helps maintain cleaner financial records.

Of course, automation alone is never enough. Every business is different, which is why human review remains essential. Simon Bookkeeping carefully reviews financial data to ensure transactions are properly categorized and aligned with each client’s business needs.

Improved Accuracy and Error Detection

One of the biggest advantages of AI technology is its ability to identify unusual patterns or inconsistencies quickly. This helps:

- Detect duplicate transactions

- Spot missing information

- Identify possible misclassifications

- Reduce manual data-entry errors

Better Financial Insights

Modern AI tools can help organize financial information into clearer reports and summaries. This allows Simon Bookkeeping to provide clients with more meaningful insights into:

- Cash flow trends

- Expense patterns

- Profitability

- Financial organization

Increased Efficiency = More Client Focus

By reducing time spent on repetitive administrative tasks, AI allows Simon Bookkeeping to dedicate more attention to client communication, support, and problem-solving.

That means clients receive:

- Faster response times

- More organized financial records

- Greater attention to detail

- More time for personalized service

Secure and Responsible Use of Technology

At Simon Bookkeeping, technology is used carefully and responsibly. AI tools are meant to assist the bookkeeping process — not replace professional oversight, confidentiality, or ethical standards.

Human judgment remains essential when reviewing financial information, understanding business context, and making bookkeeping decisions.

The Human Side Still Matters

Bookkeeping is more than software and automation. Business owners need someone they can trust to help keep their records organized and understandable.

That’s why Simon Bookkeeping combines:

- Modern technology

- Professional attention to detail

- Personalized support

- Real human communication

Looking Ahead

Technology continues to evolve, and Simon Bookkeeping is committed to staying current with tools that can improve service quality, accuracy, and efficiency for clients.

AI is not about replacing people — it’s about using smarter tools to deliver better bookkeeping support.

If you are looking for organized, modern, and reliable bookkeeping services, Simon Bookkeeping is here to help your business stay financially organized and focused on growth.